What is the future of business aviation compensation in the wake of the COVID-19 crisis?

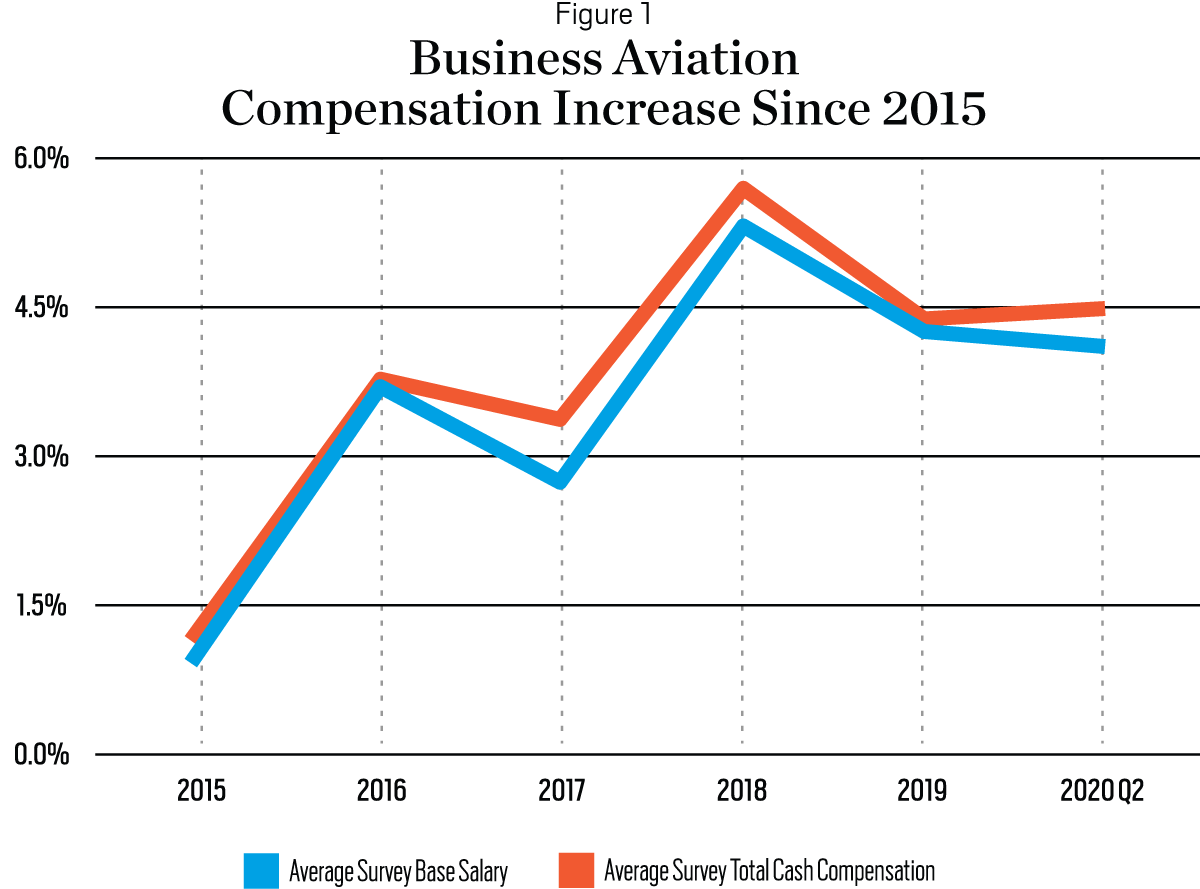

Before prognostications about where we’re going, it’s useful to understand where we’ve been. Combining the data from multiple compensation surveys, as shown in Figure 1, shows that business aviation compensation has risen an average of 3.7% per year since 2015. While there are downturns in the graph, these aren’t declines in the levels of compensation, but rather, declines in the rate of increase of compensation. That is, during the downturn years, compensation was still increasing, just not increasing at the rate of the previous year.

But there’s a problem. By the time survey data hits the street, they are already at least six months old, and reflect the compensation state of the previous year. So, survey data are reactive, not predictive, to the economic conditions that affect compensation. Survey data from this year, 2020, probably will not reflect the impact of the crisis on compensation, having been collected during the period immediately preceding and during the initial part of the COVID-19 shutdown. Odds are high that we’ll have to wait until the 2021 survey data are published before we see a reflection of that impact, assuming there is one. What do we do in the meantime?

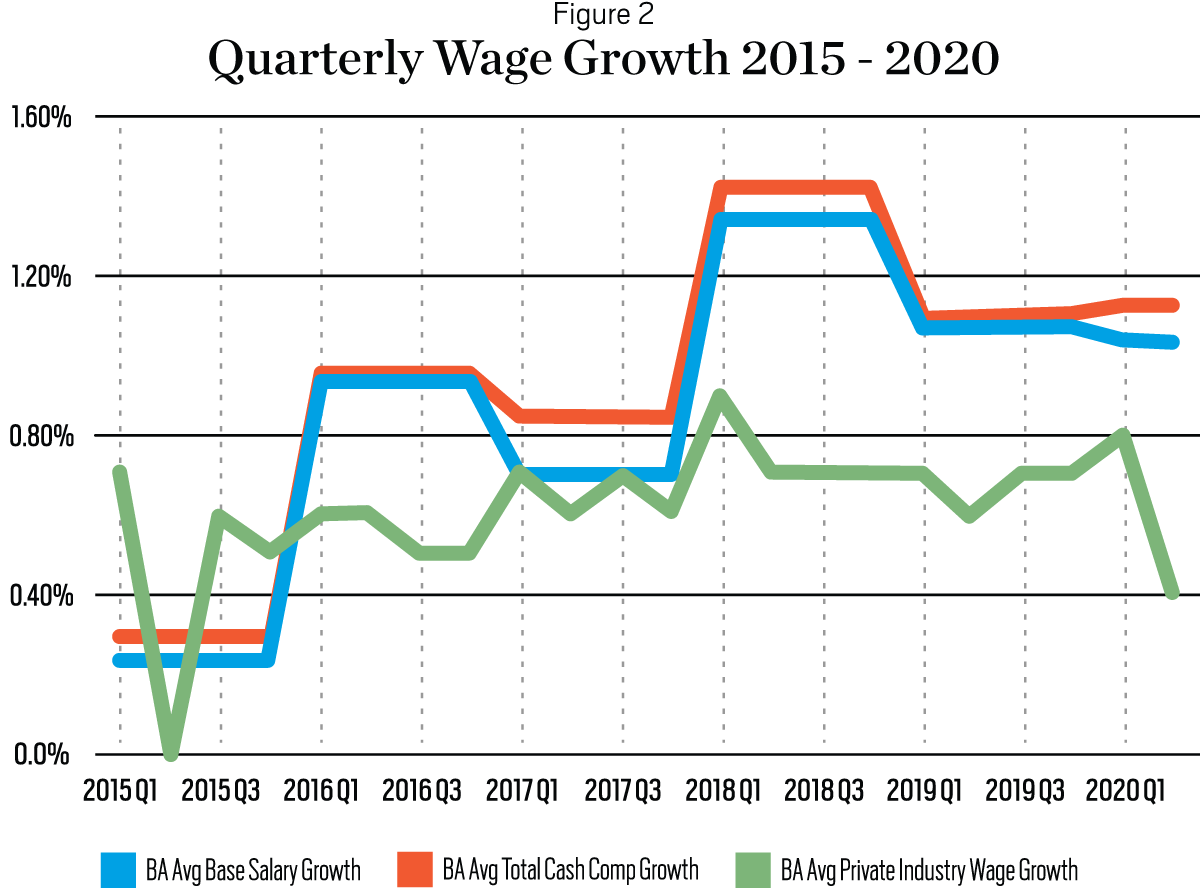

Every quarter, the Bureau of Labor Statistics (BLS) publishes a three-month statistic that provides the growth in private industry compensation. Figure 2 depicts the wage growth from Figure 1 remapped on a quarterly basis and compared against the quarterly compensation data provided by the BLS. Here, we see an interesting pattern. In nearly every case, the trend of the BLS data roughly parallels trends in survey data. In other words, because it is published more dynamically, BLS data can be a predictive indicator of the direction of survey data.

Note the BLS data for Average Private Industry Wage Growth in Q1 and Q2 of this year. In Q1, pre-COVID-19, wages were growing at a rate of .8%, but then, in Q2, that growth rate decreased to .4%. The question is: how will that decrease affect business aviation compensation in the near term? The answer doesn’t lie in specific compensation numbers, but in the compensation ranges.

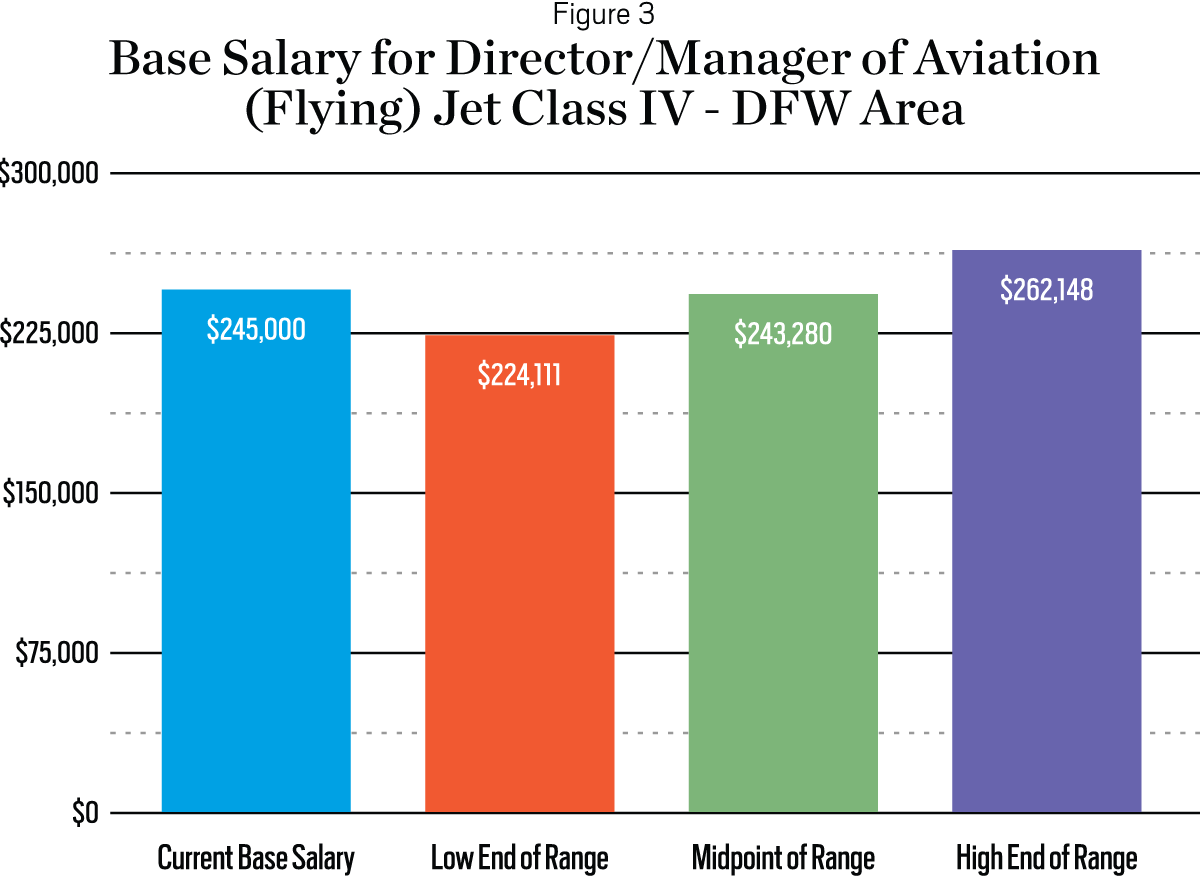

Using a proprietary methodology to analyze compensation, survey data are aged from the time of collection into the present quarter using both survey trends and data from the BLS. The aged data then are regionalized using the same tools. For any one set of conditions, several numbers are generated. The low number is the low end of the range as depicted below. The high number is the high end of the range. The results from a sample analysis are in Figure 3.

Here’s where we begin to see the impact of COVID-19. With the lower BLS wage increase statistic for Q2, the low end of the range, which typically is data aged with BLS statistics, will move lower than it was in Q1. If that same BLS statistic stays low, or goes lower, the range will continue to move lower, bringing the midpoint down as well. But the high end of the range will not change. This result will be a “flattening” of the increase trend over time, not a reversal into a decreasing trend. This pattern will be reinforced by the manner in which organizations consider the COVID-19 crisis as they review their compensation levels.

Hopefully, most operators will focus on long-term personnel retention and continue to pay competitively, not changing their compensation patterns. But some will attempt to take advantage of the crisis to hire personnel, paying them at a bargain rate. It doesn’t take Nostradamus to predict that the problem for lower-paying organizations is that when the airlines fully recover, demand for pilots will be greater than it was pre-COVID-19, and there will be a mass exodus from these organizations. BAA

Christopher Broyhill, PhD, CAM is the Founder and President of Citadel Consulting LLC. His proprietary survey data are used here, and he is the author of Business Aviation Leadership: From the Traits to the Trenches.